Budget track your way to success (Budgeting 101)

Its 2024 already, Happy New Year!

It’s great that you’re thinking about budgeting for 2024! Starting early will give you plenty of time to set realistic goals and develop a plan that works for you.

Budgeting is one of the most important aspects of financial planning that can make a difference in your overall success. It helps you manage your money, make smart spending decisions, and achieve your financial objectives. Tracking your income and expenses allows you to pinpoint areas where you can reduce spending and save more. This can be used to pay off debt, create an emergency fund, or invest in the future.

A word

In the book Atomic Habits, James Clear defines clearly how to build a habit, the most effective form of learning is practice, not planning. Focus on taking action, not being in motion. Regarding personal finance, budgeting is the first step to taking action and having a clear mindset about saving, investing, and spending. You will have the best outcomes once you make it easier to budget by using The Law of Least Effort.

Before we look into budgeting, keep in mind that your inaction to budget is the consequence of poor savings, inadequate investing, and unhealthy spending. Your inaction to ensure that you keep in motion a budget every day, every week, and every month is a direct consequence of you having to take bad loans now and then and then getting stuck in the endless cycle of having to pay up the loans and then taking another loan a minute later.

Take note your inaction has now led to you not having a clear mindset on the December festive season with money set aside through a SACCO. Just trying to picture that Christmas doesn’t cost you a leg when buying that mbuzi for your family. But that’s going to change if you follow the steps mentioned below and have the liberty to make saving and investing as frequent as you would spending.

How to budget your money

- Set realistic goals. define short-term and longer-term financial objectives. Divide your objectives into needs (rent, utilities) and desires (travel, investments).

For example: In 1-2 years (Short Term)

- I want to create an emergency fund: Aim for at least 3-6 months’ worth of living expenses.

- I want to Pay off high-interest debt.

- I want to Save for a specific purchase.

In 3-5 Years (Mid Term)

- I want to Build a solid retirement fund

- I want to Invest in education or career advancement

- I want to Reduce overall debt

In 5+ Years (Long-Term)

- I want to Achieve financial independence: Your goal should be to have enough passive income to cover your living costs, so you can retire at an ideal age or pursue other interests.

- I want to Max out my retirement savings: Make the most of your retirement savings to get the most out of your future.

- I want a Plan for estate planning: Establishing an estate plan ensures that your estate is distributed according to your wishes and minimizes tax consequences for your heirs.

- Track your income: Estimate your monthly income across all your sources. Divide your income into fixed and variable.

Make a list of these things:

- Take-home pay amount

- Passive income (Variable Income)

The first action is to journal your take-home pay. Google defines take-home pay as the money received by an employee after the deduction of tax and insurance. Point to note, if your only income is a Take-home pay, then there goes your first problem in personal finance, you have an income problem. Go back to Setting Realistic Goals and include Saving and Invest in a Passive Income channel (Diversification).

- List Your Expenses: This covers all your large and small expenses.

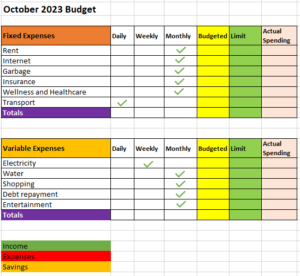

For example: Replicate an Excel sheet as shown in the image below.

N/B: I have not included Miscellaneous costs, hell yeah, you are just getting started with budget 101, money should be as finite as it can be.

Next identify your daily, weekly, and monthly recurrent costs. Your daily recurrent costs may include, Transport, Shopping, and Food. Your weekly recurrent costs may include, Electricity and Shopping and Food costs. I have included shopping and food because I know some of us ensure it is a weekly spending or even a monthly spend. Your monthly recurrent costs will then include Rent, Water Bill, Internet, Garbage, Insurance, Wellness and Healthcare (You have to take care of yourself), Debt Repayment, or Entertainment costs. You need not have the liberty to entertain yourself if say you are in a short-term loan contract. First, pay off your bad loan!

- Create the budget: Set aside a budget for each expense category, Set a limit on how much you spend on each expense category, and Don’t spend more than your income.

- Review your budget regularly: Your budget isn’t a one-size-fits-all solution. You’ll need to review and adjust it regularly to account for fluctuations in income and expenses.

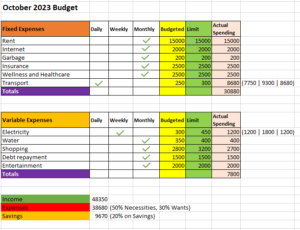

Here is an example of the final outlook by the end month.

Assumptions: Currency is in Kenyan Shillings.

A simple budgeting plan

To get the most bang for your money, I suggest following the popular 50 / 30 / 20 budget. In this budget, you spend about 50% of after-tax income on essentials, 30% on luxuries (wants), and 20% on saving and debt repayment. Once your budget is done and clear, be sure to have allocated part of the income or savings into an emergency fund, and set your goal to have enough money to cover living expenses for 3-6 months. It’s important to remember that the path to financial success is a long one. Budgeting is a great way to help you get there. You’ll have to make adjustments as you go, but if you’re proactive and disciplined with your budgeting, you’ll be well on your way to financial success. Budget tracking isn’t a road map. It’s a journey. Enjoy learning about your money and taking charge of your finances.