🚫 Debt is not your friend!

This is the reality of the Kenya we live in today, where dreams and ambitions collide with the harsh realities of financial constraints, a new phenomenon has taken root: the rise of digital loan apps. These apps promise quick, easy money at the tap of a screen, but beneath their sleek interfaces lies a web of financial pitfalls that can trap the unwary.

I remember conversing with an executive from a prominent loan app company in Kenya. Over a steaming cup of chai, he leaned in and said something that sent chills down my spine: “You know, Winnie, we dish out loans to about 60% of borrowers who end up paying our competitors.” The casual tone with which he delivered this statement belied its shocking implications. It painted a picture of a vicious cycle where desperate borrowers jump from one loan to another, sinking deeper into debt with each transaction.

This revelation underscores a crucial truth that every Kenyan needs to understand: debt is not your friend. While loans can serve a purpose in certain circumstances, the ease of access to credit in today’s digital age has led many down a path of financial ruin. Let’s explore why debt can be so dangerous and how you can navigate the treacherous waters of personal finance in Kenya’s rapidly evolving economic landscape.

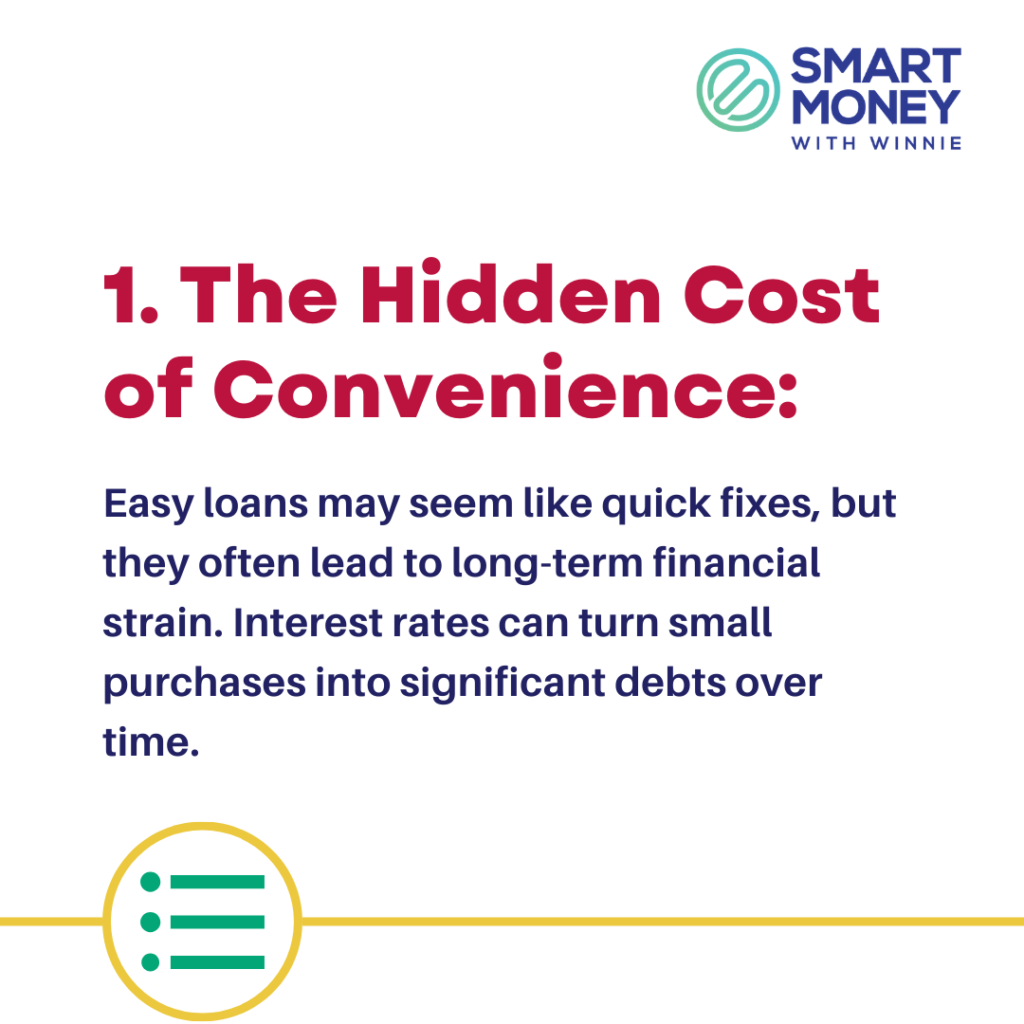

The Hidden Cost of Convenience

At first glance, digital loan apps seem like a godsend. Need 5,000 KES for an emergency? No problem. With just a few taps on your smartphone, you can have the money in your M-Pesa account within minutes. But this convenience comes at a steep price.

Consider this scenario: You borrow 10,000 KES from a popular loan app to cover an unexpected medical bill. The app charges a 10% “facilitation fee” and gives you 30 days to repay. If you can’t repay in full by the due date, you’re hit with late fees and your credit score takes a hit. Suddenly, that 10,000 KES loan has ballooned to 15,000 KES or more.

The real danger lies in the normalization of this cycle. When borrowing becomes as easy as ordering a ride-share, it’s tempting to use loans for non-essential purchases. That new smartphone or trendy outfit seems within reach, but the long-term cost can be crippling.

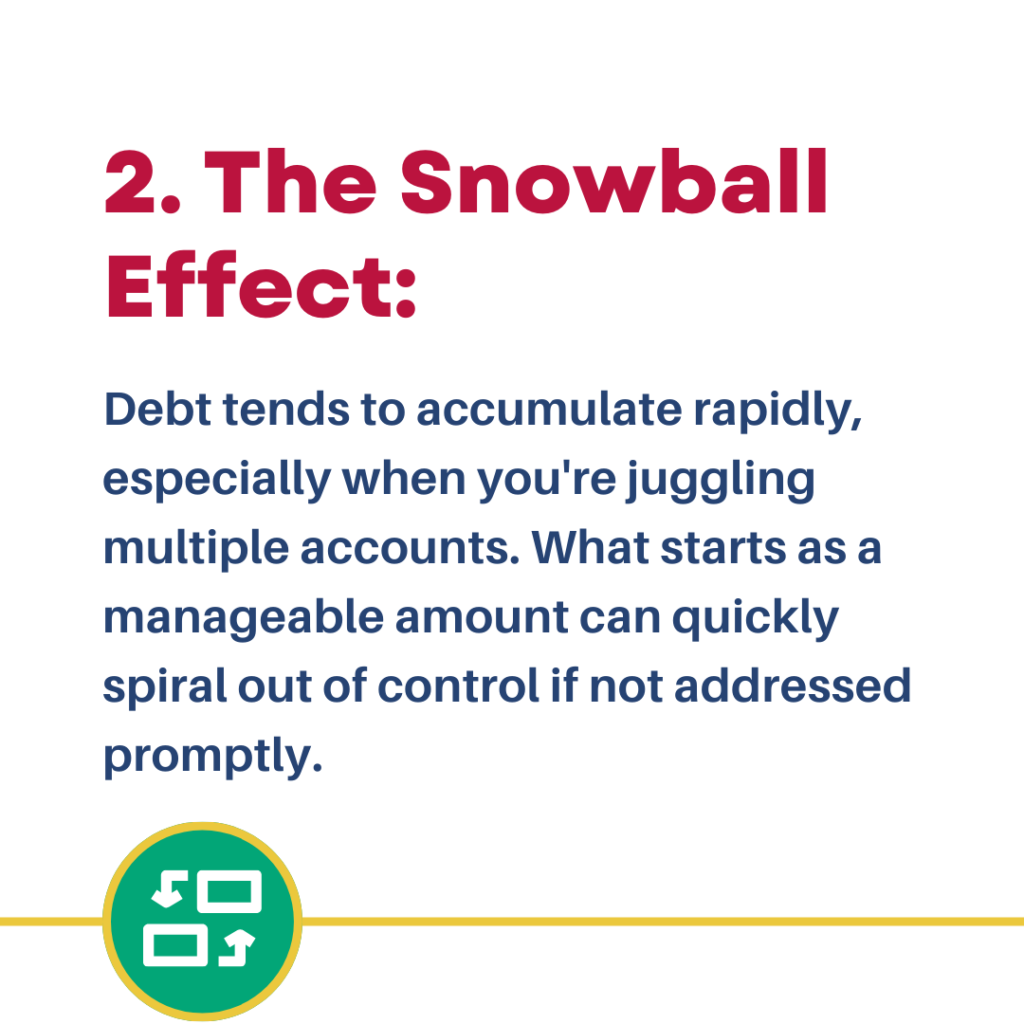

The Snowball Effect: When Debts Multiply

One loan might seem manageable, but debt has a nasty habit of multiplying. Let’s return to our executive’s revelation about borrowers using multiple apps. This practice, known as loan stacking, is alarmingly common in Kenya.

Imagine you’ve taken a 20,000 KES loan from App A. As the repayment date approaches, you realize you can’t make the payment. In desperation, you turn to App B for a 25,000 KES loan to cover the first debt and have a little extra. But now you’re on the hook for two high-interest loans. Before you know it, you’re juggling payments across multiple apps, watching helplessly as your debts snowball out of control.

This snowball effect is exacerbated by the high interest rates charged by many loan apps. Annual percentage rates (APRs) can soar into the hundreds, making it nearly impossible for borrowers to break free from the debt cycle once they’re caught in it.

The Opportunity Cost: Mortgaging Your Future

Every shilling spent repaying high-interest debt is a shilling that could have been invested in your future. This opportunity cost is one of the most insidious aspects of debt, particularly for young Kenyans trying to build a stable financial foundation.

Let’s consider two friends, Amina and Bahati. Both earn 50,000 KES per month. Amina has fallen into the debt trap and spends 15,000 KES each month repaying various loans. Bahati, on the other hand, lives within her means and invests that same amount in a diversified portfolio of stocks and government bonds.

After ten years, Amina has paid hundreds of thousands in interest and fees, with nothing to show for it. Bahati, meanwhile, has built a nest egg worth millions, thanks to the power of compound interest working in her favor rather than against her.

The opportunity cost extends beyond just money. Debt stress can lead people to postpone major life decisions like starting a family, pursuing further education, or launching a business. In this way, debt doesn’t just mortgage your financial future; it can hold your entire life hostage.

The Emotional Toll: When Money Worries Become Health Concerns

Financial stress is more than just a nuisance; it can have serious implications for your mental and physical health. Constant worry about debt can lead to anxiety, depression, and even physical ailments like high blood pressure and insomnia.

I once spoke with Maria, a 32-year-old teacher from Mombasa, who found herself 300,000 KES in debt spread across multiple loan apps. “I couldn’t sleep,” she told me, her voice shaking. “Every time my phone beeped, I thought it was another payment reminder or threat. I was scared to answer calls from unknown numbers. The stress was eating me alive.”

Maria’s story is far from unique. The shame and stigma associated with debt in Kenyan society can lead people to isolate themselves, further exacerbating mental health issues. Some even resort to desperate measures, selling assets, or engaging in risky behaviors to make loan payments.

The emotional toll of debt underscores an important truth: financial health is inextricably linked to overall well-being. Achieving financial peace of mind isn’t just about numbers on a balance sheet; it’s about reclaiming your life and your happiness.

Breaking the Cycle: The Path to Financial Freedom

Despite the grim picture painted so far, there is hope. Breaking free from the debt cycle is possible, but it requires commitment, discipline, and often a change in mindset.

The first step is to stop borrowing. This can be challenging, especially if you’ve become accustomed to using loans to make ends meet. But remember: you can’t dig yourself out of a hole by digging deeper.

Next, take stock of your debts. List out every loan, including the balance, interest rate, and due date. This can be a scary exercise, but it’s crucial for developing a repayment strategy.

Many financial experts recommend the “debt snowball” method. This involves focusing on paying off your smallest debt first while making minimum payments on others. As each debt is cleared, you roll that payment into tackling the next smallest debt. This approach provides quick wins that can help maintain motivation.

For those struggling with multiple high-interest loans, debt consolidation might be an option. Some Kenyan banks offer personal loans at lower interest rates than digital lenders. Using such a loan to pay off multiple high-interest debts can simplify your finances and potentially save you money in the long run.

Crucially, breaking the debt cycle isn’t just about repayment; it’s about changing your relationship with money. This means creating and sticking to a budget, building an emergency fund to avoid future borrowing, and learning to distinguish between needs and wants.

The Role of Loan Apps: A Double-Edged Sword

It’s important to acknowledge that loan apps aren’t inherently evil. In a country where traditional banking services are out of reach for many, these apps have played a role in increasing financial inclusion. They’ve provided access to credit for small business owners, helped people weather emergencies, and in some cases, acted as a stepping stone to more formal financial services.

However, the ease of access and lack of stringent credit checks have also led to widespread irresponsible lending and borrowing. Many users find themselves trapped in a cycle of debt, borrowing from one app to pay another.

The Kenyan government and financial regulators have begun to take notice. Recent regulations aim to curb predatory lending practices and protect consumers. But ultimately, the responsibility lies with individual borrowers to use these services wisely and understand the full implications of taking on debt.

Unsecured Loans: A Risky Proposition

Most loans offered by digital apps are unsecured, meaning they don’t require collateral. While this makes them more accessible, it also means they carry higher risk for lenders, which translates to higher interest rates for borrowers.

The lack of collateral can also lead to aggressive collection practices. Unlike traditional bank loans where defaulting might result in the seizure of an asset, digital lenders may resort to harassing phone calls, threats, or even contacting your contacts list to shame you into payment.

Moreover, unsecured loans can tempt borrowers to take on more debt than they can handle. Without a valuable asset at stake, the perceived consequences of default might seem less severe, leading to reckless borrowing.

Building a Debt-Free Future

As we wrap up this exploration of debt in the digital age, let’s return to the core message: debt is not your friend. While loans can serve a purpose in certain circumstances, they should be approached with caution and used sparingly.

Instead of relying on loans, focus on building a strong financial foundation. This includes:

- Living within your means: Create a budget and stick to it. Distinguish between needs and wants.

- Building an emergency fund: Aim to save at least 3-6 months of living expenses to avoid borrowing for unexpected costs.

- Investing in yourself: Use your resources to acquire skills or education that can increase your earning potential.

- Starting to invest early: Even small amounts invested regularly can grow significantly over time thanks to compound interest.

- Seeking financial education: Take advantage of free resources to improve your financial literacy.

Remember Maria, the teacher from Mombasa? After hitting rock bottom, she committed to turning her financial life around. It took two years of strict budgeting and focused debt repayment, but she eventually cleared her 300,000 KES debt. “The day I made my final payment, I felt like I could breathe again,” she told me, her eyes shining with pride. “Now, instead of fearing my phone, I get excited when I get a notification from my savings app.”

Maria’s story is a powerful reminder that no matter how deep in debt you might be, there’s always a path forward. It might not be easy, and it will require sacrifice, but the freedom of waiting on the other side is worth every effort.

In conclusion, as we navigate the complex world of personal finance in the digital age, let’s strive to use technology and financial innovations responsibly. Let’s build a culture of savings rather than one of borrowing. And most importantly, let’s remember that true financial freedom comes not from having access to easy credit, but from building a stable financial foundation that can weather any storm.

Your financial future is in your hands. Choose wisely, spend mindfully, and always remember: debt is not your friend.